One of Nest Realty’s founding principles is to provide full transparency of real estate information. To that end, we aim to be the definitive source for real estate data, information and analysis for the Charlottesville/Albemarle region. The Nest Report is a quarterly report that will offer data analysis and market forecasts through the eyes of experienced and progressive real estate professionals. The results of any analysis are open to interpretation, and this is one of the reasons we will provide the data in addition to our analysis.

Looking at the broad market overviews and trends provides a good bellwether for the market, but where the Nest Report differs from other reports is that we look at individual counties, not just the larger market. As you will note, the pricing history of Louisa is very different from Albemarle County. This report intends to dispel some of the myths about the wider market and provide answers to the question, “What’s going on in my market?” In addition to this Quarterly Nest Report, in coming weeks we will dive into specific neighborhoods and streets in supplemental Nest Report issues. Here in our quarterly report, we will dig down into the counties throughout the region and focus on the specific trends within these ‘sub-markets.’ First a quick area clarification: We will refer to numbers in Charlottesville City, Albemarle County, and the Charlottesville Expanded Metropolitan Statistical Area (EMSA) . The EMSA, as we are using it, includes Charlottesville, Albemarle, Fluvanna, Greene, Louisa, and Nelson. (The Government does not include Louisa in the traditional MSA, but we believe it is critical to our market.)

Where We Are: Sales Numbers

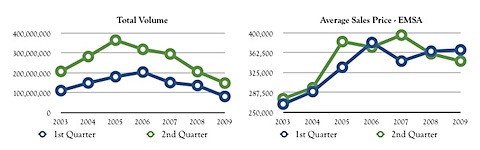

It would be a bit of an understatement to say that the real estate market is struggling. Year-over-year mid year detached home sales are down 30.1% in the Charlottesville EMSA from 957 sales in 2008 to 661 sales in 2009. Total sales volume of detached homes is also down from $347,689,720 to $234,652,420, a reduction of 32.5%. The average detached home sale price in the Charlottesville EMSA has dropped slightly from $363,312 to $354,996 (only 2.2%). So, how can sales be off 30% and the average price down just over 2%? With many of the answers in this wrap-up, you will find that in order to understand what has happened, you have to drill down to more specific data.

There are two items at play here. Product/Location Mix and Excessive Impact of Farm Sales. When you look at the specific sales driving these numbers, you find a drastic shift in what is called “Product Mix.” This refers to the percentage of homes that are selling of one type or another. In this case, the shift is a significant shift in sales from one county to another. While the overall market may have been down more than 30%, in Louisa County detached home sales were down roughly 56% and Albemarle County detached home sales were only down approximately 22%. Because Louisa’s home prices are lower on average than Albemarle, the effect of this shift in product mix is to mask some of the actual price drops.

The second item holding the average price steady are farms and estates. When the number of transactions in a quarter decreases, the impact that a single large property sale has can be quite large. In the 2nd quarter of 2009, there was a single home whose sale drove the average sales price up by more than $12,500. In years where there are 1200 transactions in the first six months, a large sale can move the market, but when the number of transactions is half that, the impact is much larger.

Now let’s take a look at detached sales in Albemarle County. The number of sales are down 22.2% (from 334 to 260) and total sales volume is down 20.8%, by a tad more than $34,000,000. Inventory of single family homes in Albemarle is now hovering right around 660. Taking into account that there have been only 260 sales of detached homes to date, this signals over a year’s worth of inventory available. As of July 1, 2008, there was actually a larger inventory, 744 detached homes; however, with the substantially larger sales numbers in 2008, there was a shorter supply in terms of time.

Within Albemarle County, the median price was down in the 2nd quarter 10.6% from the same period in 2008, from $385,000 to $344,000. The average price was up 0.7% or just less than $4,000. The difference is that single property that we referenced above. When removed from the 171 sales in Albemarle County in the 2nd Quarter, the average actually goes down $47,600 to $429,811. The effective move from 2008 to 2009 in average price is a decrease of 9.3%.

There are some potential positive signs for Albemarle detached homes. Q2 2008 sales were off by 35.5% from 2007 and mid-year 2008 total sales off 29.1%. The slide has seemingly slowed a bit with Q2 2009 sales down 19% and mid-year total sales off 22.1%. We’ll definitely keep an eye on this to see if this gives us any clues of when the market will turn around.

In the City of Charlottesville, sales seem to be decreasing at a faster rate: Single family home mid-year sales numbers are off by 35.3% and total sales volume is down by 38.5%. To date, City home sales and values have been surprisingly resilient. Mid-year sales numbers have hovered consistently between 193 and 227 from 2004 to 2008. However, they’ve definitely taken a major hit during the first half of 2009 with only 127 sales. If we compare the drop in number and value of transactions from the first half of the year in 2006 to 2009 in the city and Albemarle, we find that the city is down 44% in the number of transactions and 50% in value of transactions, and the county is down 52% for both number and volume of transactions.

Both City and County condominium sales continue to slide as well. There have been a total of 32 condos sold in the County so far (off 25.6%) and 25 sold in the City (down 46.8%). However, Charlottesville City condo sales rebounded quite well in the Q2 2009 with 22 total sales, bouncing back from a dismal Q1 which saw only 3 transactions close. There are still condo projects in front of the City Planning Department with the potential for near-future development. Whether or not those projects can obtain funding, and when they will be built is still up in the air. Additionally, we fully expect the absorption rate (time it will take for new condos to be purchased) to be lengthy compared to years past, as some of these projects are approved to include more housing units than have sold across the whole city this year.

Where We Are: Pricing

So sales numbers and total transaction volumes are down – we already knew that. Let’s dive into prices and see what the numbers are telling us. As we mentioned above, average prices for single family homes in Albemarle up 0.7% in the second quarter against the same period last year.

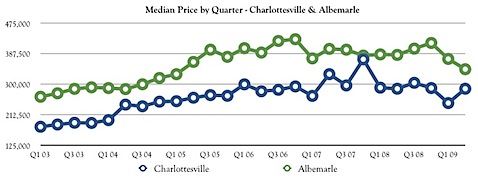

Median pricing (though it isn’t a perfect prognosticator of values) is a much better gauge for overall prices, so we’ll focus on median prices. In Albemarle, the median price of single family homes sold in Q2 2009 are 10.6% lower than those sold in Q2 2008 ($344,000 vs. $385,000). Similarly,the median price of single family homes sold in Charlottesville in Q2 2009 are 10.7% lower than 2008 ($257,250 vs. $288,000). In fact, this is the second straight year-over-year period in which the median prices of both Charlottesville and Albemarle single family homes have come down.

We maintain records of the historical median prices throughout our area. If we look backward, we have to travel to the first quarter of 2005 to find a median price equal to our current median in Albemarle County. The city is a tad harder to analyze, as the limited number of sales show a less stable course. However, the median price for the city for the first half of this year was $250,500. This would generally indicate that prices have retreated to late 2004 price points.

Condominium prices in both Charlottesville and Albemarle have also suffered. Median prices for Albemarle condos are down for the third straight time at mid-year, this time by 15.4% since 2008. Charlottesville condo median prices have been lower for two straight times at the year’s mid-point and are off by over 25% from 2008. However, we point caution into reading too much into this information. There is such a small population of condo sales that a purchasing shift from a project with lower price points such as 1800 JPA to the pricier Randolph can dramatically demonstrate a change that is not factual or realistic. One really needs to look at what units are selling and how that compares to last year.

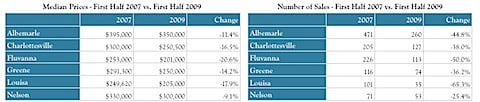

Likewise, the surrounding counties have also seen significant price drops. Median price levels from the first half of 2007 to the first half of 2009 are down in Fluvanna, Greene, Louisa, and Nelson by 20.6%, 14.2%, 17.9%, and 9.1% respectively. Number of transactions appear far more dramatic in their drops of 50%, 36.2%, 65.3%, and 25.4% for the same counties over the same time. The combination of these two drops culminates in total sales volume being off in Fluvanna, Louisa, and Nelson by more than 50%, and Greene being off by 46.5%. To put this in comparison, Charlottesville City Median Prices and Total Volume are down 16.5% and 46.2% respectively and Albemarle County Median Prices and Total Volume are down 11.4% and 43.3% respectively.

Positive Signs

1. Believe it or not, some of the best signs in the local marketplace are the drops in the median home prices. It’s clear that prices got out of control and affordability throughout Central Virginia was called into question (and rightfully so). Though there are countless external factors involved, lower prices will absolutely help the local real estate market stabilize and eventually rebound. None of us want to lose value or equity in our homes, but these price drops are getting us closer to market stabilization, and clearing supply is necessary.

2. Anecdotally, if you talk with any active Realtor in the local market, they’ll tell you that there are definitely buyers looking at properties. We don’t have access to the ‘total number of house showings’ for the entire Charlottesville EMSA, but there is a healthy flow of real buyers still in our market that are ready, willing, and able to purchase homes. Here’s the proof: approximately 1 in 3 single family homes in Charlottesville and Albemarle that have sold in 2009 were on the market for less than 30 days (32% to be exact). In fact, approximately 1 in 4 single family homes that have sold so far in 2009 went under contract in less than 2 weeks. While we’re not completely sold on the accuracy of ‘Days on Market’ (DOM) given that some Realtors attempt to ‘game‘ the system, it is a positive sign that homes do sell quickly if they are in good condition, in a good location, and priced well.

3. Lower priced homes in Albemarle County are selling. Through Q2 2008, 95 single family detached homes had sold in Albemarle County under $300,000. In 2009, 94 have sold by the year’s mid point. It’s been said that lower-priced homes are selling…and it’s true. In fact, it’s not uncommon for great homes that are priced well to have multiple offers. Whether it’s the $8000 first-time homebuyer tax credit or the fact that home prices have come down some (or probably a combination of the two), homes at the lower price points are still selling quite well. (This will be the focus of the first Nest Report Supplement next week.)

Lending Environment

If there is any single frustration that buyers and real estate professionals on both sides of transactions can agree on is that the banking industry is a mess. Most agents will tell you that loans are simply not being approved in a timely manner, and that even when they are, loans are still not closing smoothly.

Early this year, the new HVCC (Home Valuation Code of Conduct) (link to pdf) was put into place by the NY Attorney General’s office and adopted by Fannie Mae. Many of the provisions of the HVCC seem harmless, but in practice are making the lending process extremely difficult. There is now a middle man between banks and appraisers, and the two are no longer allowed to speak to one another. Established to protect the appraisers from influence of the banks, this Chinese wall means that when problems occur, there is almost no efficient way to make corrections or clarifications.

New practices that we have to look forward to will require that any change in the HUD-1 (the official government form tracking costs in home sales) will require a three day review process for all parties involved. This sounds good, until you realize that most HUD-1s are completed the day of closing. We are being told by lenders that escrows for repairs will no longer be allowed. Repairs will need to be made, and the bank will need verification of the repair. If there is a change in the APR, this will require a three day waiting period while the borrower reviews the costs. Keep in mind that an APR will change if an appraisal costs $50 more than anticipated, or if the title insurance is not sold for the exact price estimated.

While there are buyers looking to buy, and sellers looking to sell, the current lending environment is such that fewer and fewer home sales will occur on the date expected by both parties. Buyers and sellers alike should make contingency plans early on in the event that a home does not sell in a timely manner.

On the interest rate front, things are outstanding. Provided that you can make your way through the lending maze and that you can qualify for a loan, rates are favorable. Even jumbo loans offer interest rates that are attractive. Currently, some federal lenders are offering jumbo rates in the low 5s with few points. As of this writing, conventional rates are around 5.125 with a single point. To put this rate in perspective, a borrower who purchases a house for $375,000 (roughly our EMSA median price) today at 5.125% with 20% down, would pay $361 (>22%) a month less than a buyer of the same house at 7.00% interest.

Market Forecast

We may be on a road to recovery, but it is looking like a long road, and we are not quite there yet. Though there are a scattering of positive signs in the local real estate market, there are too many unknowns to think that things are going to turn around next week.

The biggest unknown that our market, and every other market in the country, is dealing with is potentially rising unemployment. Area unemployment has doubled in the last 12 months, going from 3.0% to 5.9%. It’s the highest unemployment numbers in the Charlottesville MSA in years. Unemployment numbers are too important to dismiss; that’s why we don’t think that we can even talk about a market turnaround until national and local unemployment numbers stabilize and jobs start being created (instead of being lost). On the bright side, the Charlottesville unemployment numbers are lower than the national (9.1%) and state (7.0%) numbers.

Foreclosures will continue to play a larger role in our local real estate market for the remainder of 2009 and likely much of 2010. It’s clear that foreclosures have been on the rise from 2007 to today. A lack of a good source of information prevents us from providing anything objective here. You can be sure that appraisers will be forced to use these foreclosures as comparables and it will make bank approval and financing even more of a struggle for arms length market transactions. (This has been happening in Northern Virginia…and it’s starting to trickle towards us).

There are indications that new construction ‘starts’ may start to ramp up again in the Fall of 2009. Several builders have been able to secure land at deep discounts across Central Virginia. Coupled with the fact that labor and materials costs have come down, builders can now afford to build new homes with lower asking prices than they have been able to for several years. This savings should make its way to the buyer and there will be relative values in new construction soon. Hence, this ‘reduced’ new home pricing will create more inventory and competition and will most likely push re-sale home pricing down in many areas throughout Charlottesville, Albemarle, Louisa, Greene, and Fluvanna.

Based on conversations we’ve had with several builders, they are planning to concentrate on building new homes in what they have referred to as a ‘sweet spot’ of around $300,000. So, expect re-sale values of competing homes to suffer a bit in that price range. Also, since there are several builders all targeting this market, we expect some ‘pricing wars’ between builders in late 2009 and early 2010 if the demand is less than anticipated.

Expect high priced and luxury properties to be hit the hardest in the coming months. Albemarle County currently has 108 active listings for properties priced at or above $1,000,000 and 17 have sold YTD – that translates into approximately 3 years’ worth of million dollar inventory. There are also 60 active single family properties in Albemarle between $750,000-$999,999 with 19 sales YTD. Last year, the credit markets severely affected low and medium priced homes. So far in 2009, numerous factors have directly affected the high end market. Overall economic conditions, the tightening of jumbo loan accessibility, and the shortage of ‘move-up’ buyers have all slowed higher priced home sales. Nationally, the National Association of Realtors states that there is a 40-month supply of homes over $750,000.

The hardest hit million dollar homes have been and will continue to be those in neighborhoods and subdivisions. Through July 1, there have been 2 sales of million-plus homes in Albemarle County on less than 2 acres and both were pre-sold ‘custom’ homes. There are, however, 5 currently under contract in this category (2 in Ednam, 1 each in West Leigh, Ednam Forest, and Ashcroft). Yet, there are 21 single family homes of this type currently listed for sale.

Interest rates have been stable for a few months, with a few exceptions, but few can expect these rates to stay as low as they are. Fear of inflation will force the Fed to take action over the next year to begin ratcheting them up. A 1% move from today’s rate has the effect of moving monthly payments up more than 11%. This could result in cutting off the entry level buyers, or it could drive prices further downward. An uptick in demand will be needed to hold prices steady.

Don’t expect a turnaround in the next few months. We anticipate sales will continue to lag. However, we may see a slight year-over-year increase during the second half of 2009, but only because 2008 2nd half sales numbers were so poor. Until unemployment bottoms and consumer confidence starts to rise, we anticipate a shaky market. It’s true that we may need to sort through more foreclosures and short sales in order to stabilize the market, but unemployment rates are the #1 key to track. Until large employers including local governments, The University and private industry begin hiring additional employees, it is doubtful that we will see any meaningful and positive changes to the unemployment numbers.

Summary

If you are a buyer: there are (and will continue to be) deals to be had. Do your research, be patient, and buy smart. For sellers, it’s all about location, price, and condition. You’ve got to have 2 of the 3 going for you. If you are in a so-so location, then your home has to be in immaculate condition and priced right. If you are in a great location, you need to be priced right or your home better be in great condition. We should all be thankful that we are in an area where there still are jobs and buyers (even though there aren’t as many as there used to be). Because of that, if you really want to (or need to) sell your home, you probably can..

For the full Nest Report as a PDF with full-size charts and graphs , download it here.

Nest Realty Group Market Reports by Nest Realty Group, LLC is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License. Based on a work at nestrealtygroup.com. Permissions beyond the scope of this license may be available at http://nestrealtygroup.com.

Nest Realty Group Market Reports by Nest Realty Group, LLC is licensed under a Creative Commons Attribution-Share Alike 3.0 United States License. Based on a work at nestrealtygroup.com. Permissions beyond the scope of this license may be available at http://nestrealtygroup.com.

Nest Real Estate Group's 2009 Mid-Year Market Report for Charlottesville, Virginia region | Real Central VA

Written on

[…] Nest Realty Group released our first mid-year market report. Personally, I am excited about this because it represents one of the reasons we originally […]

Bruce Lemieux

Written on

I didn’t know that a font this small existed — can’t read the article.

Jim Duncan

Written on

Working on it …

Jim Duncan and Keith Davis Talk Charlottesville Real Estate

Written on

[…] The Nest Report Nest Realty's blog, The Nest Report, is a platform to educate the public about the changing Charlottesville real estate market, including community news, industry updates, market reports, and all of the great things Charlottesville, Albemarle County, and Central Virginia have to offer. « Nest Realty Group’s Mid-Year 2009 Market Report […]